Owning rental properties in Indiana comes with real financial rewards-and real financial risks. Tenant damage, liability lawsuits, and lost rental income can wipe out your profits fast.

Residential landlord insurance Indiana protects your investment by covering property damage, liability claims, and income loss when tenants can’t pay rent. We at Shurr Insurance help landlords understand what coverage they actually need.

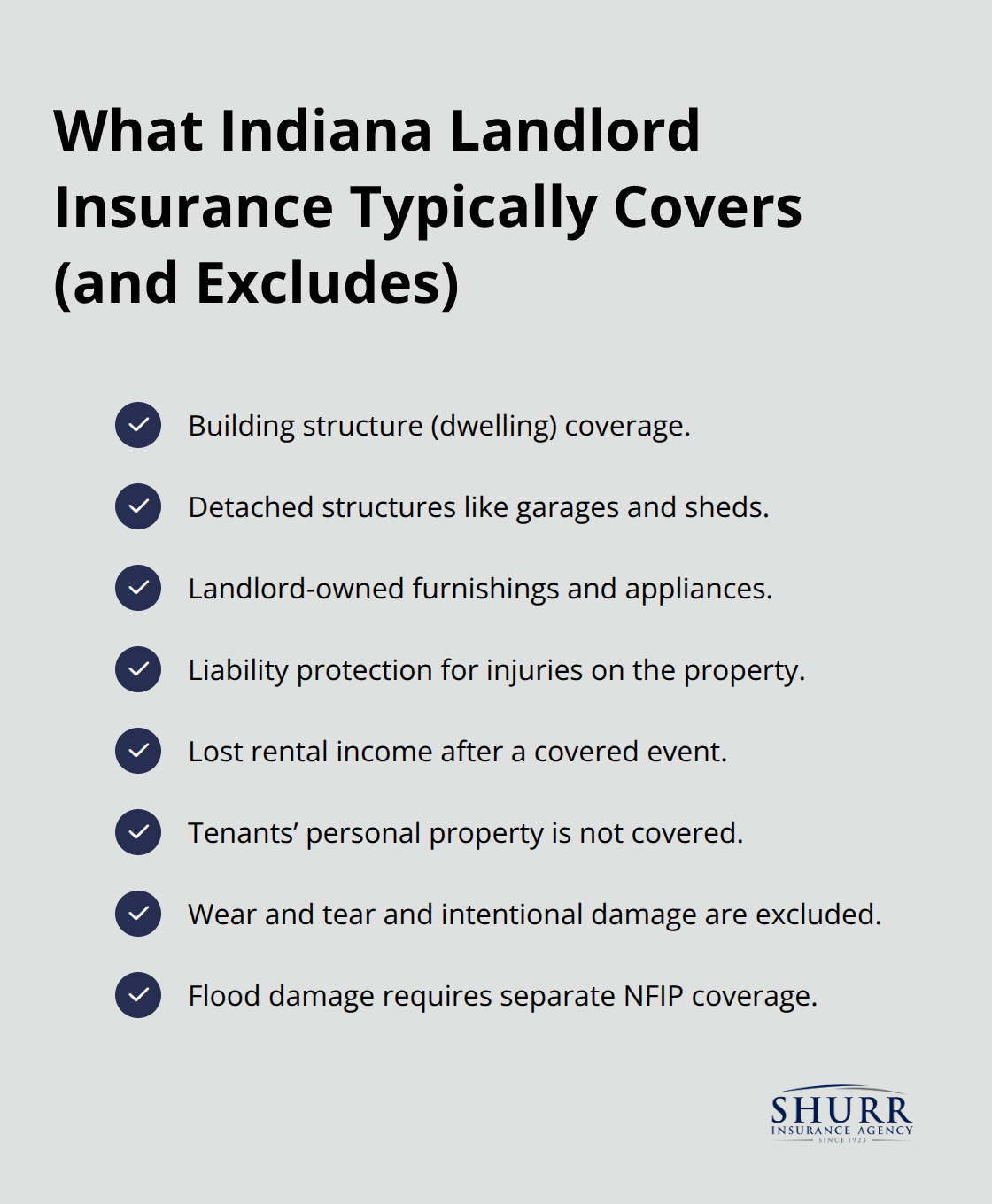

What Landlord Insurance Actually Covers

Residential landlord insurance in Indiana differs fundamentally from homeowners insurance, and that distinction protects both your wallet and your legal standing. The policy covers the building structure itself, any detached structures like sheds or garages, your own furnishings and appliances at the rental property, liability claims when someone is injured on the property, and lost rental income if a covered event forces tenants to vacate. Standard policies do not cover your tenants’ personal belongings-that responsibility falls to them through renters insurance-and they do not cover normal wear and tear, intentional damage by tenants, or flooding (which requires separate flood insurance through the National Flood Insurance Program).

Understanding Your Premium and Priority Coverages

The median Indiana landlord insurance premium runs around $1,069 per year, placing the state in the lower-middle range nationally. Your actual cost depends heavily on property location, age, construction type, expected monthly rent, and local weather and crime risk. Roof and exterior damage from hail and severe storms represent the most common claims in Indiana, so wind and hail coverage should rank high in your policy review. Properties in areas with higher tornado frequency or hail risk will see premiums reflect that exposure.

Loss of Rent Coverage Protects Your Income Stream

Loss of rent coverage protects your income stream when disaster strikes. If a fire, burst pipe, or other covered event makes the property uninhabitable, this coverage reimburses the rental income you would have collected while repairs happen. Without it, you lose money twice: once from the damage itself and again from the months your unit sits vacant during reconstruction. Indiana landlords with tight cash flow margins cannot afford gaps in income, especially when replacement costs for rebuilt property often exceed the original purchase price by 20 to 30 percent due to materials, labor, and current building code requirements.

Liability Coverage Shields You From Lawsuits

Liability coverage is equally non-negotiable. Medical payments coverage and legal liability protection shield you from lawsuits and medical costs if a tenant or visitor is injured on the property, with typical limits ranging from $300,000 to $2 million per occurrence and adding roughly $200 to $400 per year to your premium. Indiana’s fast eviction process and lack of rent control mean your income can evaporate quickly without solid protection. These two coverages-loss of rent and liability-form the foundation of any landlord policy. Understanding what each covers positions you to evaluate policies that actually match your risk profile and income needs.

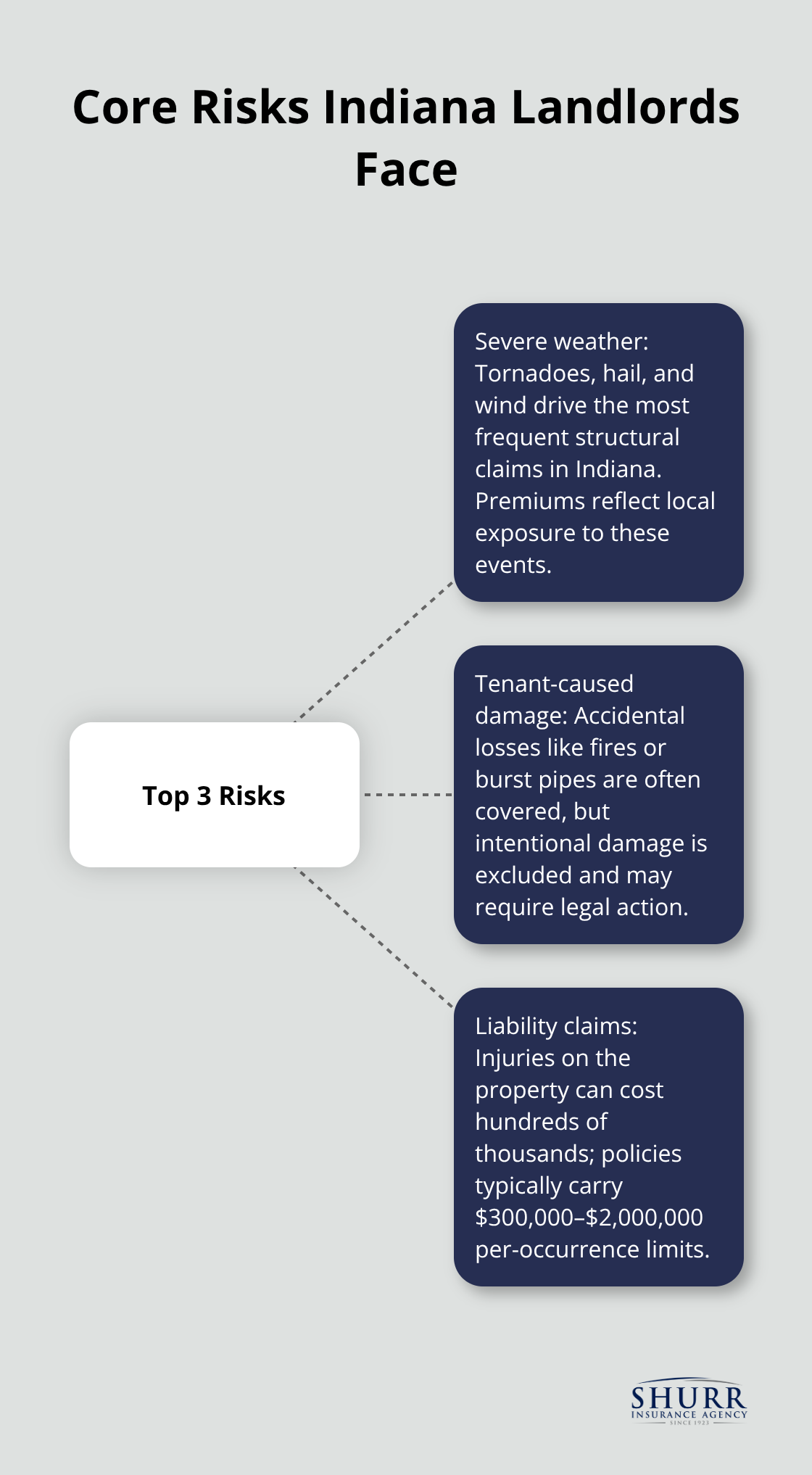

Common Risks Landlords Face in Indiana

Severe Weather Threatens Your Property Structure

Indiana landlords confront three distinct threats that standard homeowners insurance simply will not cover. The National Weather Service records an average of 22 tornadoes annually in Indiana, plus recurring hail and flooding in the Ohio River basin, making severe weather the leading cause of landlord claims in the state. Roof and exterior damage from hail strikes and wind represent the most frequent losses, which is why wind and hail coverage cannot be an afterthought in your policy selection. A single hail event can cause tens of thousands in damage to roofing and siding, and because Indiana experiences this risk repeatedly each year, insurers price policies accordingly.

Tenant-Caused Damage Creates Costly Exposure

Beyond weather, tenant-caused damage creates a second major exposure. Accidental damage like a kitchen fire or burst pipe from tenant negligence typically receives coverage under your policy, but intentional damage does not, which means you would need to pursue legal action against the tenant to recover costs-a lengthy and expensive process. Thorough tenant screening and requiring renters insurance from all occupants form essential risk management, not optional extras. This approach protects your income and reduces the likelihood that you’ll face uninsured losses from tenant actions.

Liability Claims Can Reach Hundreds of Thousands

Liability claims form the third critical risk. If a tenant or visitor is injured on your property due to a maintenance issue, poor lighting, or unsafe conditions, you face medical bills, legal defense costs, and potential settlements that can reach hundreds of thousands of dollars. Indiana’s fast eviction timeline means property problems can escalate quickly if not addressed, and a single slip-and-fall lawsuit can wipe out years of rental income. The liability coverage in your landlord policy typically ranges from $300,000 to $2 million per occurrence, but understanding your actual exposure based on property condition and traffic volume determines whether these limits are adequate.

Why These Risks Demand Proper Coverage

These three risks-severe weather causing structural damage, tenant negligence creating costly repairs, and visitor injuries triggering lawsuits-are not theoretical concerns for Indiana landlords. They happen regularly, and they happen to properties that lack proper coverage. Understanding how to evaluate policies that address each of these exposures directly shapes whether your rental investment survives a major loss intact. The next section walks you through the specific steps to select a policy that covers your actual risk profile.

How to Choose the Right Landlord Insurance Policy

Calculate Your Property’s True Replacement Cost

Start by calculating your property’s replacement cost, not its purchase price. This single step separates landlords who recover fully from losses and those who face financial devastation. Replacement cost means what it would actually cost to rebuild your property today with current materials and labor, plus compliance with modern building codes. Contact local contractors or use available cost estimators to get realistic figures for your specific area and property type. Once you know this number, choose your coverage form carefully and use it as your dwelling coverage limit. Underinsuring by even $20,000 means you absorb that gap out of pocket when a major loss occurs.

Assess Your Furnishings, Appliances, and Liability Exposure

Next, assess what furnishings and appliances you provide. If you supply a refrigerator, stove, washer, and dryer, add coverage for those items. If you rent the unit unfurnished, this coverage becomes minimal. Your liability limit should reflect your property’s traffic and condition. A well-maintained single-family home in a quiet neighborhood might justify $300,000 in liability coverage, but a multi-unit property or one with known maintenance issues warrants the $2 million limit. Indiana’s fast eviction process means problems escalate quickly, so erring toward higher liability protection costs relatively little but protects substantially more.

Collect Quotes From Multiple Carriers

Collecting quotes from at least three different carriers reveals the real price variation in Indiana’s market. Travelers, Progressive, Stillwater Insurance Group, Safeco, and Foremost all serve Indiana landlords, and their rates differ based on how they evaluate risk. One carrier might charge $950 annually while another quotes $1,300 for the same property, so skipping this comparison costs real money. Request quotes online or work with an independent agent who can access multiple carriers simultaneously.

Compare Coverage Details and Deductible Options

When comparing quotes, look beyond the premium alone. Check whether wind and hail coverage is included or requires an endorsement, since hail damage ranks among Indiana’s most frequent claims. Verify that loss of rent coverage has no waiting period before payments begin and confirm the daily benefit amount matches your actual monthly rent. Review the deductible structure carefully. A $1,000 deductible costs less than a $500 deductible, but only choose the higher amount if you can absorb that out-of-pocket cost without strain. Indiana landlords with limited cash reserves should stick with $500 deductibles despite the slightly higher premium.

Unlock Savings Through Discounts and Bundling

Ask about discounts that lower your final cost. Installing a functioning security system, smoke detectors, or a sprinkler system can lower premiums by 10 to 15 percent. Bundling your landlord policy with personal auto or home insurance often yields 15 to 25 percent savings across all policies combined. These discounts matter far more than the base premium when making your final decision.

Final Thoughts

Residential landlord insurance in Indiana protects your investment when damage, liability claims, or lost income threaten your cash flow. The three core risks facing Indiana landlords-severe weather damage, tenant-caused losses, and liability lawsuits-demand coverage that matches your property and income needs. Calculating your replacement cost, assessing your liability exposure, and comparing quotes from multiple carriers separates landlords who recover fully from losses and those who face financial devastation.

Contact an independent insurance agent who understands Indiana’s rental market and can access multiple carriers simultaneously. An agent identifies gaps in coverage you might miss on your own and finds discounts that lower your final cost. We at Shurr Insurance have served Northwest Indiana since 1923, and our team knows the specific risks landlords face in this state (we represent many of the best insurance companies in the industry and work to build long-term relationships by placing your protection first).

Proper landlord insurance delivers long-term benefits that extend far beyond a single claim. It protects your income stream when tenants cannot occupy the property, shields you from liability lawsuits that could wipe out years of rental profits, and gives you peace of mind that your investment survives major losses intact. Contact Shurr Insurance today to discuss your specific property and coverage needs.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation