Restaurant kitchens in Indiana face real financial risks every day. Fire, equipment failure, and food spoilage can shut down operations and drain your profits fast.

At Shurr Insurance, we know that eateries kitchen coverage Indiana protects you against these costly losses. The right policy keeps your business running when things go wrong.

Real Kitchen Risks That Cost Indiana Restaurants Money

Fire and Equipment Failures Drive Massive Losses

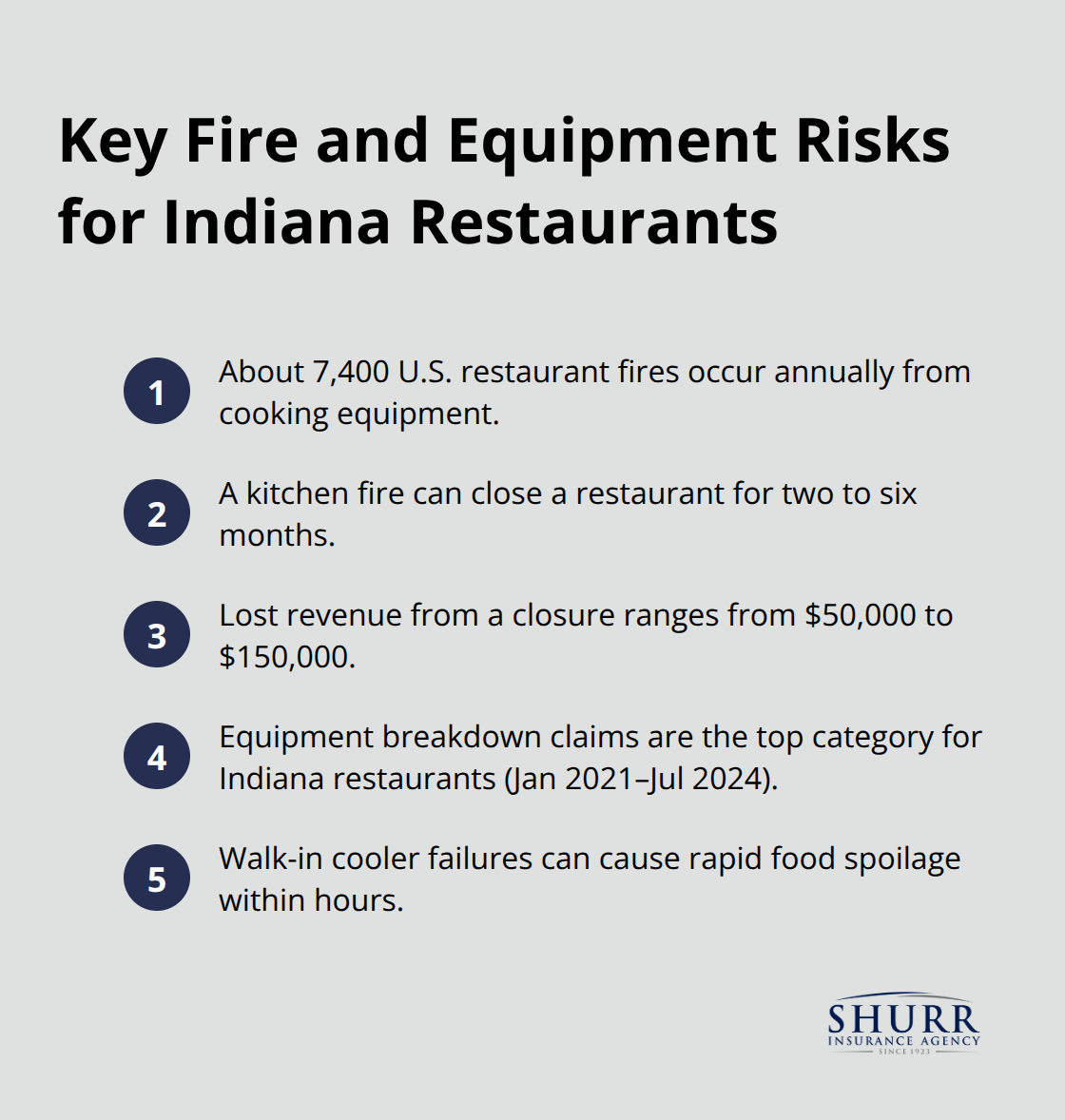

The National Fire Protection Association reports about 7,400 U.S. restaurant fires annually caused by cooking equipment, with grease fires accounting for the majority. A single kitchen fire forces a restaurant to close for two to six months, resulting in lost revenue between $50,000 and $150,000. Indiana restaurants face this exact threat every operating day, and standard property insurance often leaves critical gaps. Equipment breakdown claims represent the top claim category for Indiana restaurants according to data from January 2021 through July 2024, meaning your ovens, refrigerators, and HVAC systems fail more frequently than most operators realize.

When a walk-in cooler stops working, you lose inventory fast-spoilage wipes out thousands of dollars in food costs within hours.

Employee Injuries and Kitchen Accidents Add Up Quickly

Beyond fire and equipment failure, Indiana restaurants experience constant exposure to employee injuries and customer accidents tied directly to kitchen operations. The Bureau of Labor Statistics reports a non-fatal injury rate of about 5.5 per 100 full-time workers annually in foodservice, with cuts representing 25 percent of injuries averaging around $1,800 per claim and fractures exceeding $22,800. Slip and fall accidents happen constantly in restaurants, with wet floors near bathrooms and kitchen exits creating liability exposure that a single serious injury can amplify significantly. These numbers matter because they reflect your actual risk profile, not theoretical scenarios.

Standard Property Insurance Leaves You Exposed

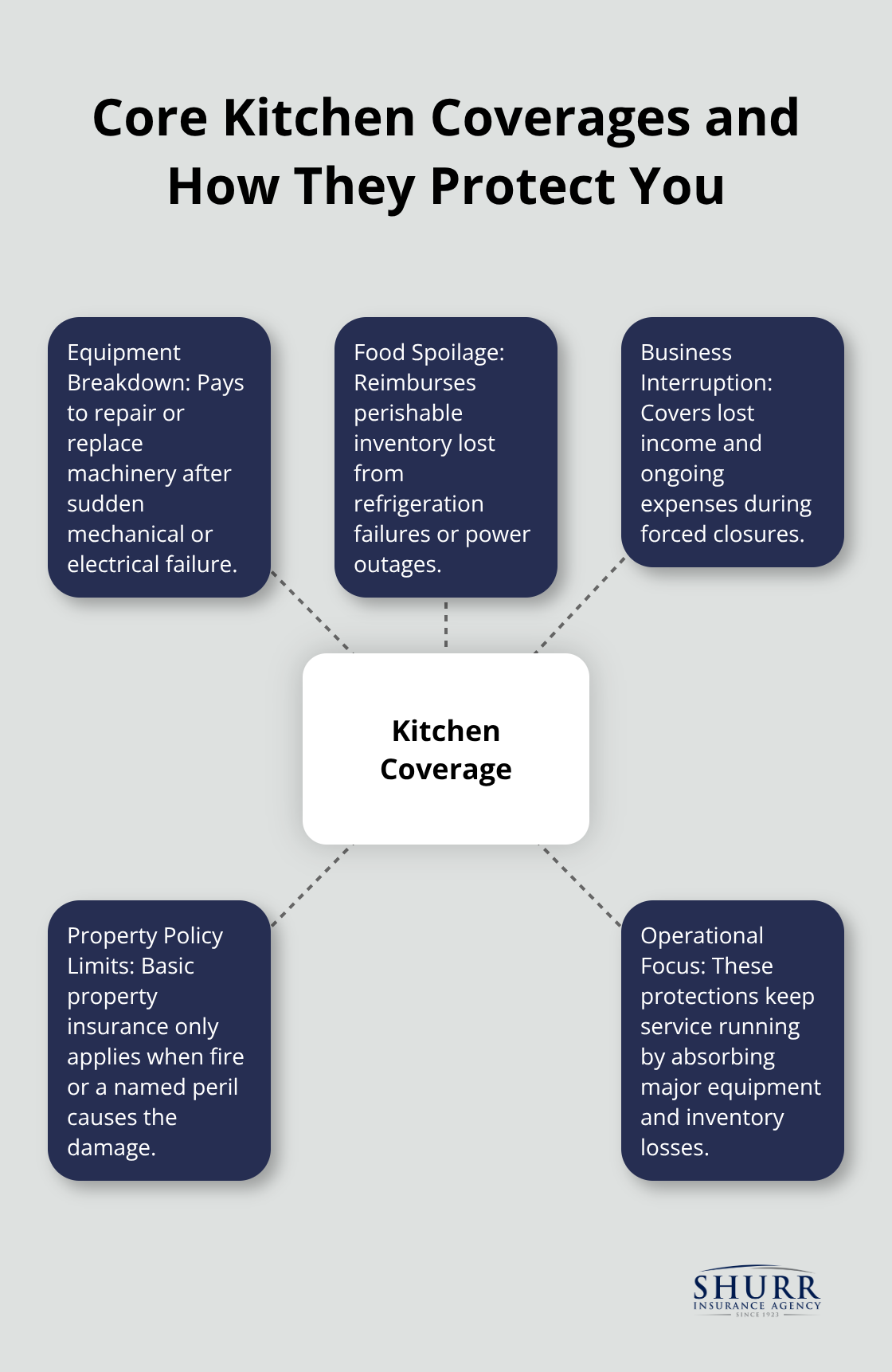

Standard property insurance excludes equipment breakdown coverage, meaning sudden failures of refrigeration, ovens, and HVAC systems fall outside protection. This gap leaves you exposed to repair or replacement costs that can reach tens of thousands of dollars. Food spoilage coverage is separate and essential-it reimburses inventory lost from refrigeration failures or power outages, a real risk for kitchen operations storing perishable goods. Business interruption insurance covers lost income and ongoing expenses during forced closures, protecting your cash flow when a kitchen fire or major equipment failure halts service. Without this coverage, you absorb the full financial impact while your competitors continue operating.

Liquor Liability and Cross-Border Complexity

Liquor liability adds another layer if you serve alcohol-Indiana’s proximity to Kentucky creates cross-border regulatory complexity that increases exposure beyond standard general liability limits. Equipment breakdown, spoilage, liquor liability, and business interruption bundled together typically cost $3,000 to $10,000 annually, a modest investment compared to the $50,000 to $150,000 cost of a three-month kitchen closure. Understanding what your current coverage actually protects leads directly to identifying which specific kitchen protections your restaurant needs most.

What Your Kitchen Coverage Actually Protects

Equipment Breakdown Covers What Property Insurance Misses

Equipment breakdown coverage pays for repairs or replacement of critical kitchen machinery after sudden failures-the exact gap that standard property policies leave wide open. Your walk-in refrigerator, commercial oven, HVAC system, and ice machine are not covered under basic property insurance when they fail mechanically; fire or a named peril must damage them for coverage to apply. When a refrigerator stops working, spoilage coverage kicks in to reimburse the inventory lost within hours, protecting thousands of dollars in perishable food.

Food spoilage coverage stands completely separate from property insurance and covers inventory loss from refrigeration failures, power outages, or equipment breakdowns-a distinction most operators miss until they experience a loss.

Business Interruption Protects Your Cash Flow During Closures

Business interruption insurance reimburses your lost income and ongoing operating expenses during forced closures from kitchen fires, equipment failure, or other covered events. A three-month kitchen closure costs $50,000 to $150,000 in lost revenue according to the National Fire Protection Association, and business interruption coverage absorbs that financial blow while you repair or replace equipment. This protection matters most when a major failure halts service for weeks or months, keeping your business afloat when revenue stops but bills continue arriving.

Liability Coverage Addresses Kitchen-Specific Employee and Customer Risks

Liability coverage for kitchen-related accidents protects you from bodily injury claims when employees cut themselves, slip on wet floors, or suffer burns-cuts alone represent 25 percent of foodservice injuries with average claims around $1,800, and fractures exceed $22,800 per claim based on OysterLink research. Your general liability policy covers customer slip-and-falls in dining areas and third-party injuries, but kitchen-specific liability focuses on employee exposures and operational hazards. If you serve alcohol, liquor liability coverage protects against dram shop claims when a customer is injured after consuming alcohol at your establishment, and Indiana’s proximity to Kentucky adds regulatory complexity that standard general liability policies do not address.

Bundling Coverages Saves Money and Closes Gaps

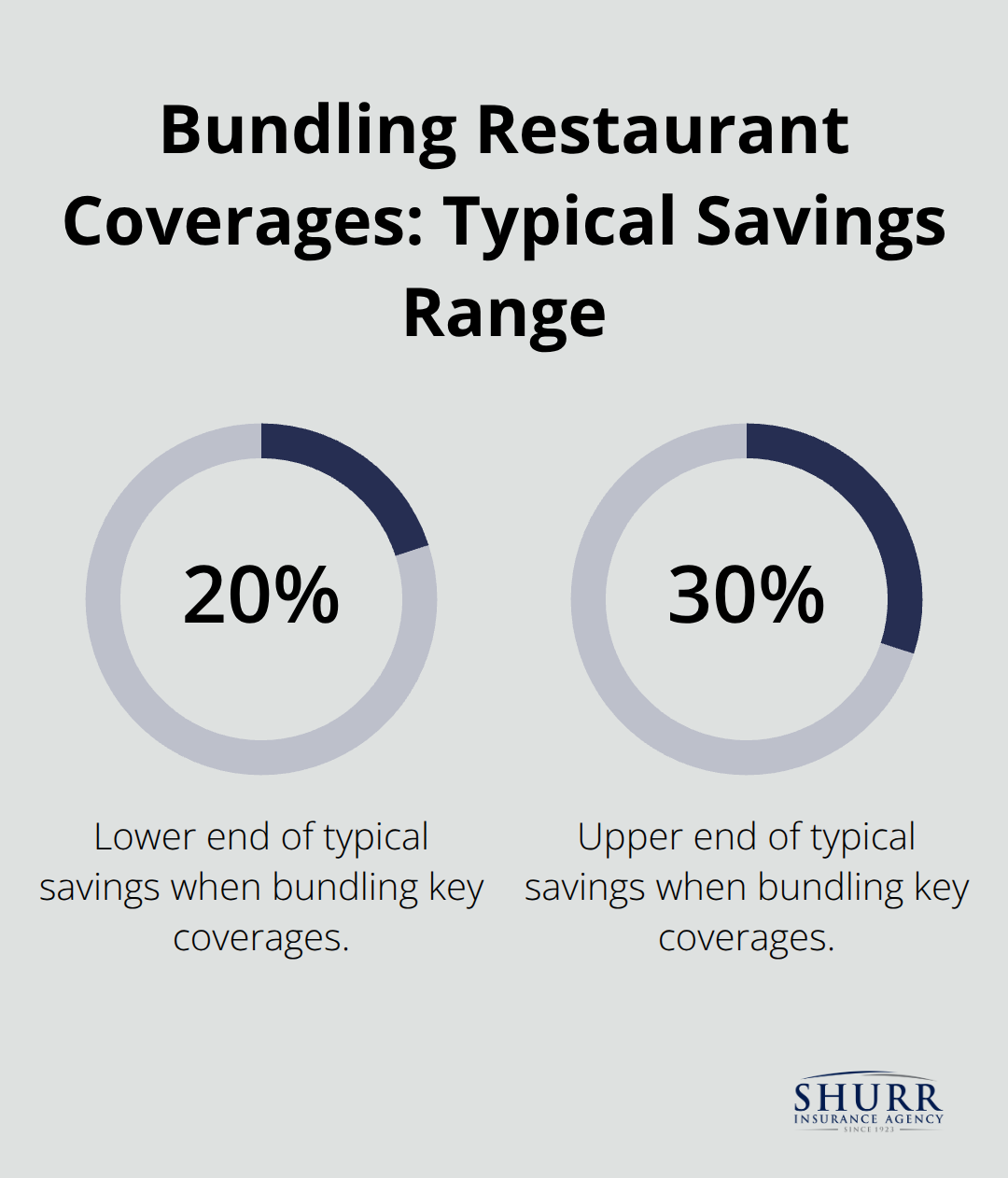

Equipment breakdown, spoilage, liquor liability, and business interruption bundled together typically cost $3,000 to $10,000 annually and save 20 to 30 percent compared to purchasing coverages individually. Bundling also prevents the coverage gaps that emerge when operators buy policies separately from different carriers, leaving overlaps and exposures unprotected.

An independent agent can assemble a coordinated program tailored to your specific kitchen equipment, inventory value, and operational model-whether you operate a traditional full-service kitchen, a ghost kitchen, or a hybrid delivery operation. The right combination of these protections transforms your kitchen from a financial liability into an insured asset, allowing you to focus on operations rather than catastrophic loss scenarios. Understanding which coverages apply to your specific kitchen equipment and risks leads directly to identifying the right policy limits and deductibles for your restaurant’s actual exposure.

Choosing Kitchen Coverage That Matches Your Restaurant

Inventory Your Equipment and Calculate Real Values

Start with an honest inventory of what you actually own and what can actually fail. Walk through your kitchen with a notepad or phone and list every piece of equipment: walk-in coolers, commercial ovens, fryers, ice machines, HVAC systems, and any specialized equipment tied to your menu. Note the age and condition of each item because older equipment fails more frequently, and Indiana buildings with aging electrical systems and gas lines face heightened breakdown risk. Calculate your monthly food inventory value by multiplying your average weekly purchase amount by 4.3, then multiply that by the number of weeks you typically hold perishable stock. This number determines your spoilage coverage limit. If you serve alcohol, identify your annual liquor revenue because carriers price liquor liability based on alcohol sales, not total revenue. Most operators underestimate their equipment value by 30 to 40 percent, which leads to underinsurance and denied claims when failures occur.

Gather Documentation Before You Request Quotes

Collect your lease or mortgage documents, employee count, annual sales figures, and a detailed equipment list so you have concrete numbers ready when comparing quotes. This preparation prevents carriers from making assumptions about your operation and ensures accurate pricing. Carriers need specifics about your kitchen setup, not estimates or rough figures. The more detailed your information, the more precise your quotes become.

Request Quotes with Identical Coverage Terms

Reject any quote that bundles coverage without showing line-item pricing for equipment breakdown, spoilage, business interruption, and liability separately. A cheap bundled quote that excludes food spoilage or carries low liquor liability limits creates false savings that evaporate the moment a loss occurs. Request three to five quotes with identical coverage limits, deductibles, and endorsements so you see true pricing differences rather than coverage gaps disguised as lower premiums. Equipment breakdown coverage should cover your walk-in refrigeration and cooking equipment with repair or replacement cost limits matching your actual equipment values. Spoilage coverage limits should equal at least one month of perishable inventory, and business interruption should cover your fixed monthly expenses plus lost profit for a reasonable closure period (typically 90 days).

Understand Realistic Pricing for Your Operation

For a small two-employee restaurant package including general liability, workers compensation, and property coverage, expect to pay around $359 monthly according to industry benchmarks, with bundled equipment breakdown and spoilage adding roughly $250 to $850 monthly depending on equipment value and inventory levels. These figures help you evaluate whether quotes fall within normal market ranges or represent unusual pricing. Bundled coverage typically saves 20 to 30 percent compared to purchasing policies individually, so factor this discount into your comparison.

Work with an Independent Agent for Market Access

An independent agent accesses multiple carriers simultaneously, compares options side by side without rebuilding applications for each carrier, and re-shops the market annually when your operation changes or premiums rise. This approach beats shopping online because independent agents advocate during claims and tailor coverage to Indiana’s specific liability landscape rather than applying templated policies designed for national markets. Agents also identify coverage gaps that online quote tools miss, ensuring your kitchen protection actually matches your real exposures.

Final Thoughts

Kitchen coverage protects your restaurant from the financial devastation that fire, equipment failure, and food spoilage create. Equipment breakdown, spoilage, business interruption, and liability coverage work together to absorb these costs, keeping your operation solvent when disaster strikes. The data confirms this reality: equipment breakdown represents the top claim category for Indiana restaurants, employee injuries average $1,800 to $22,800 per incident, and a three-month kitchen closure costs $50,000 to $150,000 in lost revenue.

Choosing the right eateries kitchen coverage Indiana requires honest assessment of your equipment values, inventory levels, and operational risks. Most operators underestimate their actual exposures and end up underinsured, discovering coverage gaps only after a loss occurs. Gathering detailed documentation about your kitchen equipment, employee count, and annual sales prevents this mistake by ensuring carriers price your actual risk rather than making assumptions.

An independent agent transforms this process from overwhelming to straightforward. We at Shurr Insurance build long-term relationships with restaurant owners and identify risks that online quote tools miss, representing multiple carriers and tailoring coverage to Indiana’s specific liability landscape. Contact Shurr Insurance today to assess your kitchen coverage and close the gaps that standard policies leave exposed.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation