Running a restaurant in Indiana means facing real liability risks every single day. From foodborne illness claims to slip-and-fall accidents, one incident can threaten your business financially.

Foodservice liability insurance in Indiana protects you when customers get hurt or property gets damaged at your establishment. We at Shurr Insurance help restaurant owners understand what coverage they need and how to get properly protected.

The Three Liability Risks That Cost Indiana Restaurants the Most

Foodborne illness outbreaks represent the single largest financial threat to Indiana restaurants. The CDC estimates that roughly 1 in 6 Americans (or 48 million people) gets sick from foodborne illnesses annually, and when your restaurant is the source, the consequences are severe. A contamination incident triggers lawsuits exceeding $75,000 to $250,000 in defense and settlement costs alone. Beyond legal expenses, a foodborne illness outbreak spreads rapidly through social media, damaging your reputation in ways that traditional insurance cannot fully repair.

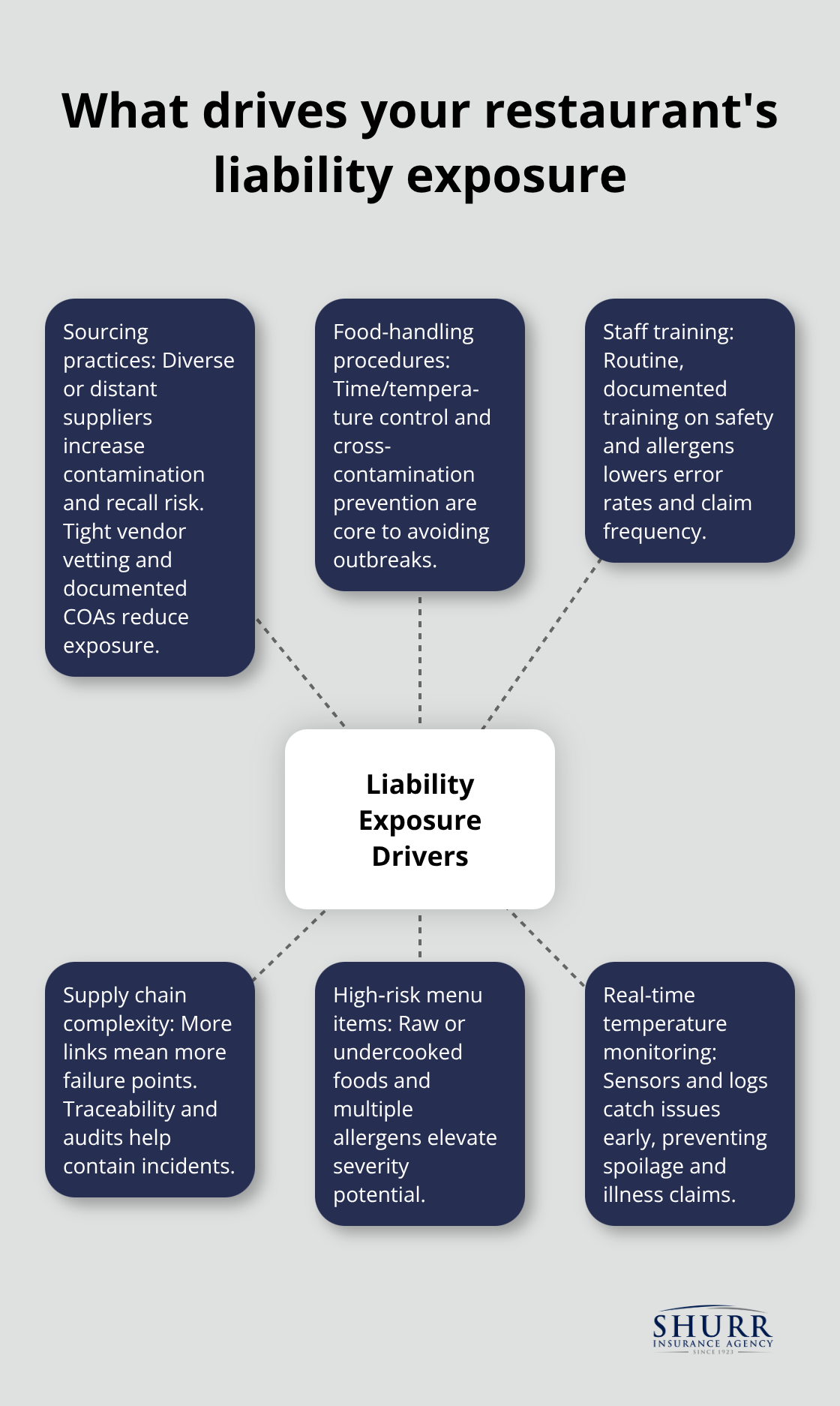

Product liability insurance specifically covers contamination claims that general liability policies exclude, making it non-negotiable for any Indiana foodservice operation. Your sourcing practices, food-handling procedures, and kitchen staff training directly influence your exposure level. Restaurants with complex supply chains or high-risk menu items face elevated premiums, but investing in food safety protocols and real-time temperature monitoring systems can lower your rates while preventing incidents.

Slip-and-Fall Accidents Drive Major Claims

The Bureau of Labor Statistics reports a nonfatal injury rate of 5.5 per 100 full-time foodservice employees annually, meaning a restaurant with 20 staff members will likely experience at least one serious injury each year. Slip-and-fall accidents in kitchens and dining areas generate significant liability claims because customers and employees both pursue legal action.

A serious slip-and-fall settlement typically ranges from $75,000 to $250,000 when medical costs and legal defense combine. General liability insurance covers these third-party and employee injury claims, but the coverage works differently depending on whether the injured party is a customer or an employee. Keeping walkways clear, maintaining dry floors, and installing slip-resistant surfaces reduces risk substantially. Your insurance agent should review your premises layout and safety procedures to identify high-risk zones and recommend targeted improvements that lower premiums while protecting people.

Allergic Reactions and Ingredient Mishandling Create Hidden Exposure

Ingredient mishandling and undisclosed allergens trigger claims that restaurants often underestimate. A customer experiencing an allergic reaction from cross-contamination or mislabeled ingredients can pursue both general liability and product liability claims. Staff training on allergen protocols, clear menu labeling, and documented ingredient sourcing become critical risk-management tools.

Insurers increasingly reward restaurants that implement allergen-management systems and maintain detailed training records. Understanding your specific menu items, preparation methods, and ingredient sourcing practices helps you identify coverage gaps before an incident occurs. An independent insurance agent who understands Indiana foodservice operations can guide you toward the right protection for your operation’s unique risk profile.

What Foodservice Liability Insurance Actually Covers

Foodservice liability insurance protects your restaurant from the financial fallout of customer injuries and property damage claims, but understanding what sits inside and outside your coverage matters far more than knowing the policy name. General liability covers third-party bodily injury when a customer slips on a wet floor or bites into contaminated food, paying for their medical bills, legal defense costs, and court settlements up to your policy limits. The average general liability claim for a serious slip-and-fall or burn injury runs $75,000 to $250,000 according to industry data, which means your policy limits should reflect the actual exposure in your restaurant. If you carry only $300,000 in limits and face a major foodborne illness outbreak affecting multiple customers, you face personal liability for amounts exceeding your coverage. Property damage liability within your general liability policy covers damage your restaurant causes to someone else’s property, though this applies less frequently in typical restaurant operations than bodily injury claims.

Why Product Liability Stands Apart from General Liability

General liability explicitly excludes foodborne illness and contamination claims, which is why product liability insurance stands as a separate necessity, not an optional add-on. Product liability specifically covers claims arising from contaminated food, undisclosed allergens, or foreign objects in meals, addressing the exact incidents that cause the largest financial losses in Indiana restaurants. When the CDC estimates 48 million Americans get foodborne illnesses annually, and a single outbreak can generate defense and settlement costs exceeding $75,000 to $250,000, leaving this gap uninsured amounts to gambling with your business. Your product liability policy should include crisis-management resources and reputation-protection services because social media spreads food-safety incidents faster than any traditional communication channel.

How Defense Costs and Medical Expenses Stack Up

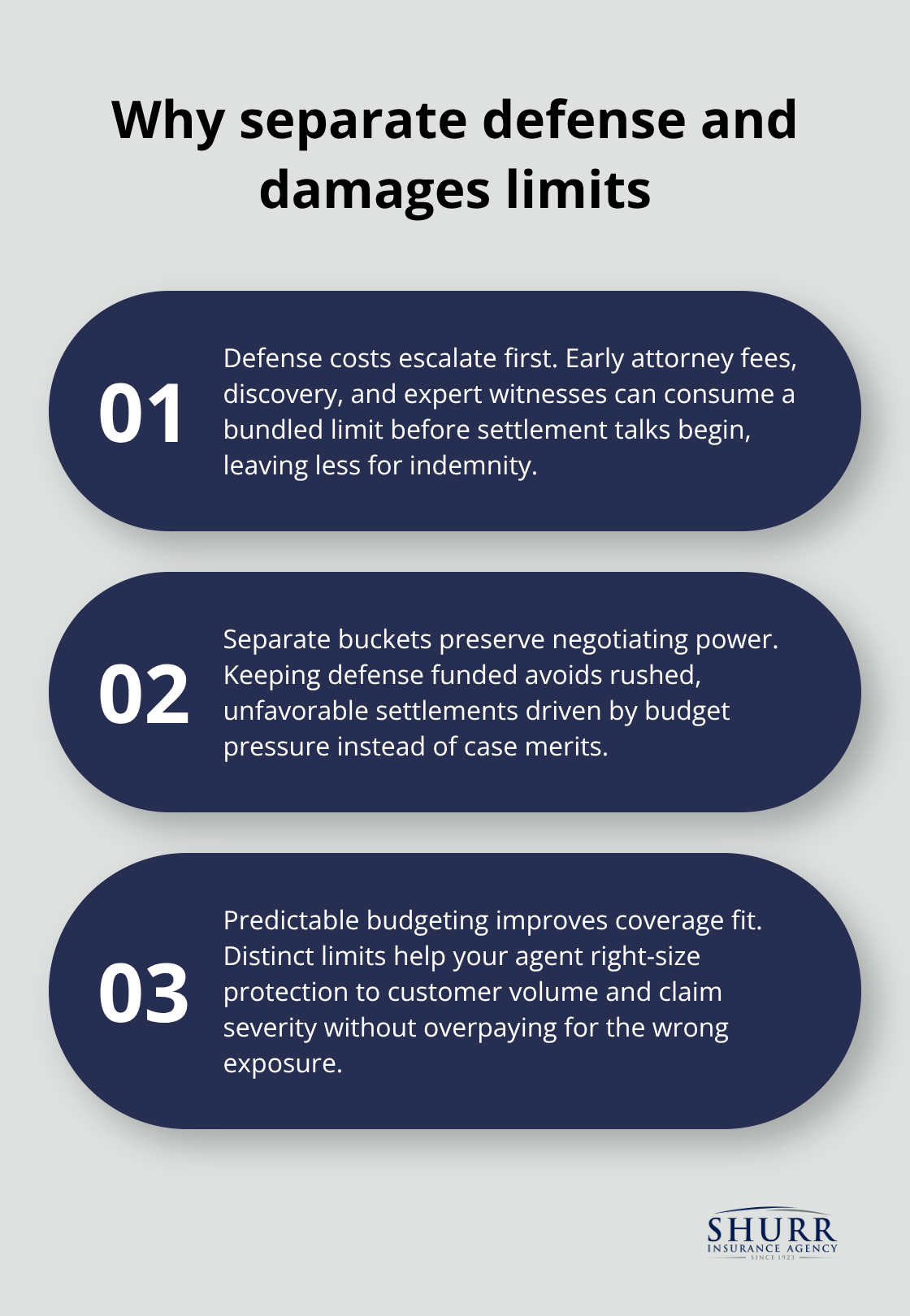

Legal defense costs and medical expenses consume claim dollars quickly, so policies covering both defense and damages separately provide stronger protection than policies bundling them under a single limit. A serious contamination incident or slip-and-fall accident triggers immediate legal expenses that mount before any settlement occurs. Separating defense coverage from damage limits means your restaurant’s defense team stays fully funded while settlement negotiations proceed, preventing budget constraints from forcing unfavorable agreements.

An independent insurance agent familiar with Indiana foodservice operations can size your limits based on your customer volume, menu complexity, and supply chain practices rather than applying generic industry minimums.

Sizing Coverage to Match Your Restaurant’s Actual Risk

Your restaurant’s liability exposure depends entirely on what you serve, how many customers you handle daily, and where your operation sits within Indiana’s foodservice landscape. A quick-service burger joint with 15 employees faces fundamentally different risks than a full-service steakhouse with 50 staff members and a complex supply chain spanning multiple regional suppliers. Start by documenting your annual customer volume, number of employees by role, whether you prepare food on-site or receive pre-made items, and your delivery footprint if applicable. Indiana’s over 13,000 restaurants generate roughly $19.1 billion in annual sales across wildly different risk profiles, so generic coverage limits fail most operators.

Setting General Liability Limits Based on Customer Volume

Your general liability limits should reflect realistic exposure based on your customer count and claim history. A restaurant serving 200 customers daily faces higher aggregate exposure than one serving 50, which means policy limits of $500,000 per occurrence and $1 million aggregate represent a reasonable starting point for mid-sized operations. Larger establishments should carry $1 million per occurrence or higher to protect against serious slip-and-fall or contamination claims that can reach $75,000 to $250,000 in defense and settlement costs.

Assessing Product Liability Exposure

Product liability limits deserve equally careful assessment because a single foodborne illness outbreak affecting multiple customers can exhaust inadequate coverage. If you source ingredients from 10 different suppliers and prepare complex dishes with multiple allergens, your product liability limits should exceed $500,000 per claim. A simple menu with limited ingredient sourcing may function adequately with lower limits, though higher protection makes sense given the financial stakes involved in food safety incidents.

Comparing Policies Across Multiple Carriers

Comparing policies across multiple insurers reveals dramatic differences in what actually gets covered despite similar-sounding names. One insurer’s general liability policy might include liquor liability coverage while another requires a separate endorsement, creating cost and coverage gaps if you don’t read the fine print. Request detailed coverage documents from at least three insurers and compare exclusions explicitly, not just premiums. Equipment breakdown coverage, spoilage protection for refrigeration failures, and business interruption limits vary significantly between carriers, and missing even one of these can cost tens of thousands when equipment fails or a kitchen fire forces closure.

Leveraging Specialized Insurance Agents

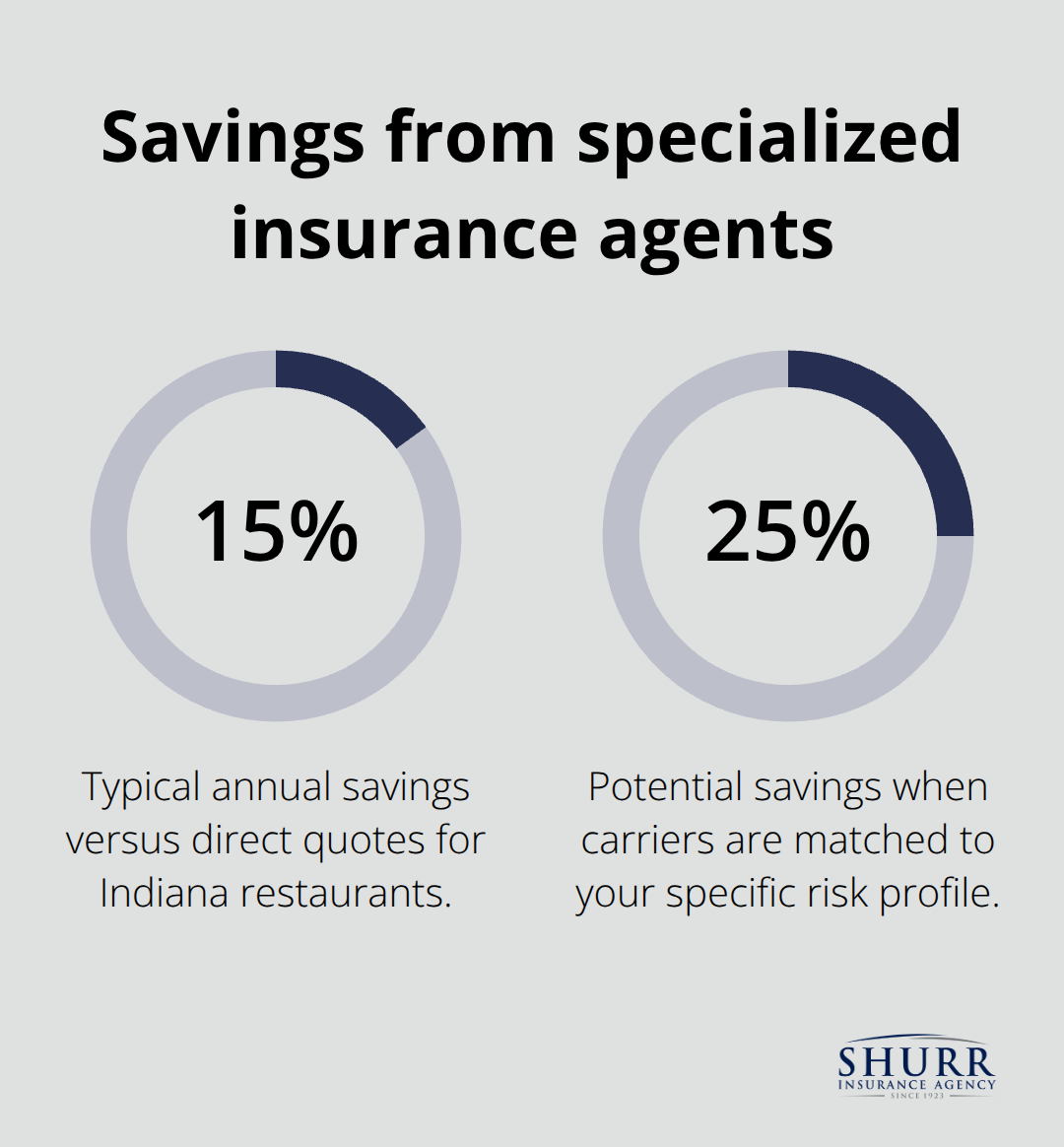

The National Fire Protection Association reports roughly 7,400 restaurant fires annually in the United States, with grease fires dominating, meaning equipment breakdown and business interruption coverage should top your priority list. An independent insurance agent who specializes in Indiana foodservice operations will shop multiple carriers simultaneously rather than steering you toward one company’s standard package. This approach typically saves restaurants 15 to 25 percent annually compared to direct quotes because specialized agents understand which carriers offer the best rates for your specific risk profile and can negotiate better terms based on loss history and safety investments.

Final Thoughts

Foodservice liability insurance in Indiana protects your restaurant from the financial devastation that follows a serious incident. Whether a customer suffers a slip-and-fall accident, experiences a foodborne illness, or encounters an undisclosed allergen, your liability coverage stands between your business and potentially catastrophic losses. The risks are real, the costs are substantial, and the consequences of underinsurance extend far beyond immediate legal expenses into lost revenue, damaged reputation, and operational disruption.

Securing adequate liability coverage starts with honest assessment of your operation’s actual exposure. Document your customer volume, employee count, menu complexity, and supply chain practices, then use this information to set realistic policy limits rather than accepting generic industry minimums. An independent insurance agent who specializes in Indiana foodservice operations shops multiple carriers simultaneously and negotiates better terms based on your specific risk profile and loss history, typically saving restaurants meaningful money annually while ensuring your coverage actually matches your operation.

We at Shurr Insurance have served Northwest Indiana since 1923, and our team understands the specific risks facing Indiana foodservice operators. Contact us today to discuss your foodservice liability insurance needs and build a protection plan tailored to your restaurant’s unique operations.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation