If you own a business with vehicles, understanding how commercial auto insurance works is essential. Your coverage protects your company from liability, property damage, and other risks that come with operating company vehicles.

At Shurr Insurance, we help business owners navigate their coverage options and find policies that match their actual needs. This guide breaks down the basics so you can make informed decisions about protecting your business.

What Counts as Commercial Auto Insurance

Coverage for Business Vehicles

Commercial auto insurance covers vehicles that your business owns or leases when they’re used for work purposes. This includes box trucks, service vans, work vehicles, and even standard cars if employees drive them on company business. The coverage protects your company from liability claims when someone is injured or property is damaged due to an accident involving your business vehicle. It also covers physical damage to your own vehicle from collisions, theft, or vandalism.

Why Personal Auto Insurance Falls Short

The key difference from personal auto insurance is that commercial policies are built for business operations, not just commuting. Personal policies explicitly exclude business use, which means if an employee gets into an accident while making a work delivery or visiting a client, your personal auto policy will deny the claim. This gap leaves your business exposed to significant financial risk.

When Your Business Needs Commercial Coverage

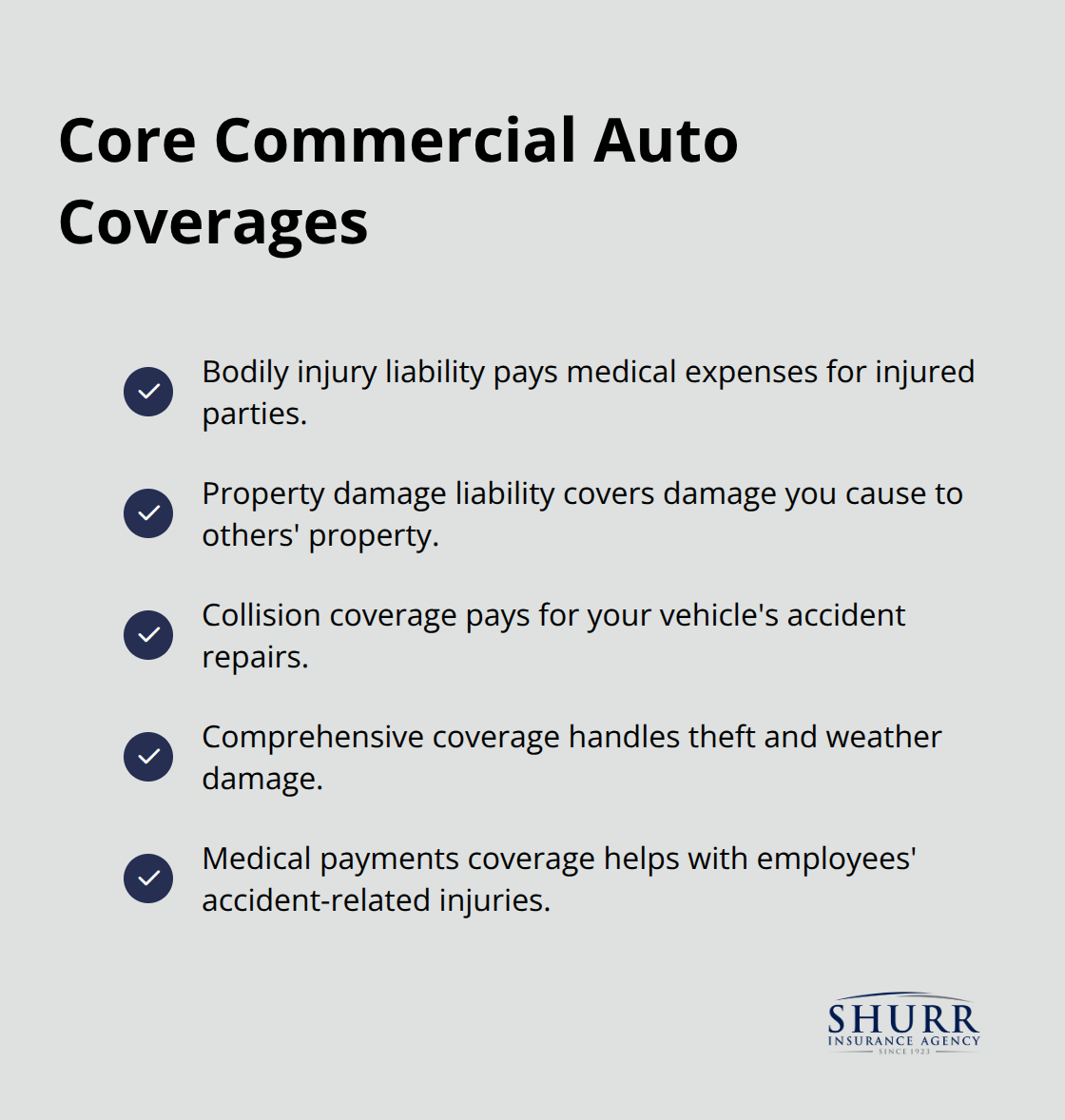

You need commercial auto insurance if your business owns vehicles, if you lease vehicles for work, or if employees regularly use vehicles to perform job tasks like transporting goods, delivering services, or visiting multiple job sites. If your business entity owns the vehicle, commercial coverage is required in nearly all cases. The coverage includes bodily injury liability to pay medical expenses for injured parties, property damage liability to cover damage you cause to someone else’s property, collision coverage for accidents with other vehicles, comprehensive coverage for theft and weather damage, and medical payments coverage for your employees’ accident-related injuries.

What Affects Your Premium

Your premiums depend heavily on driving history, vehicle type and weight, the number of vehicles in your fleet, your industry’s risk profile, and your claims history. A small business with one driver typically pays significantly less than a larger operation with multiple vehicles and drivers. Some policies also include uninsured motorist coverage if the at-fault driver lacks sufficient insurance. The Hartford and other major insurers offer these core protections, though coverage specifics vary by policy.

Getting the Right Guidance

If you’re unsure whether your situation requires commercial coverage, an independent agent who understands your specific business operations can make the decision clear and help you avoid paying for unnecessary coverage or leaving gaps in protection. Your agent will assess how your vehicles operate, who drives them, and what risks your business actually faces. This assessment determines which coverage types you truly need and which optional protections make sense for your operation.

What Drives Your Commercial Auto Insurance Rate

How Insurers Calculate Your Premium

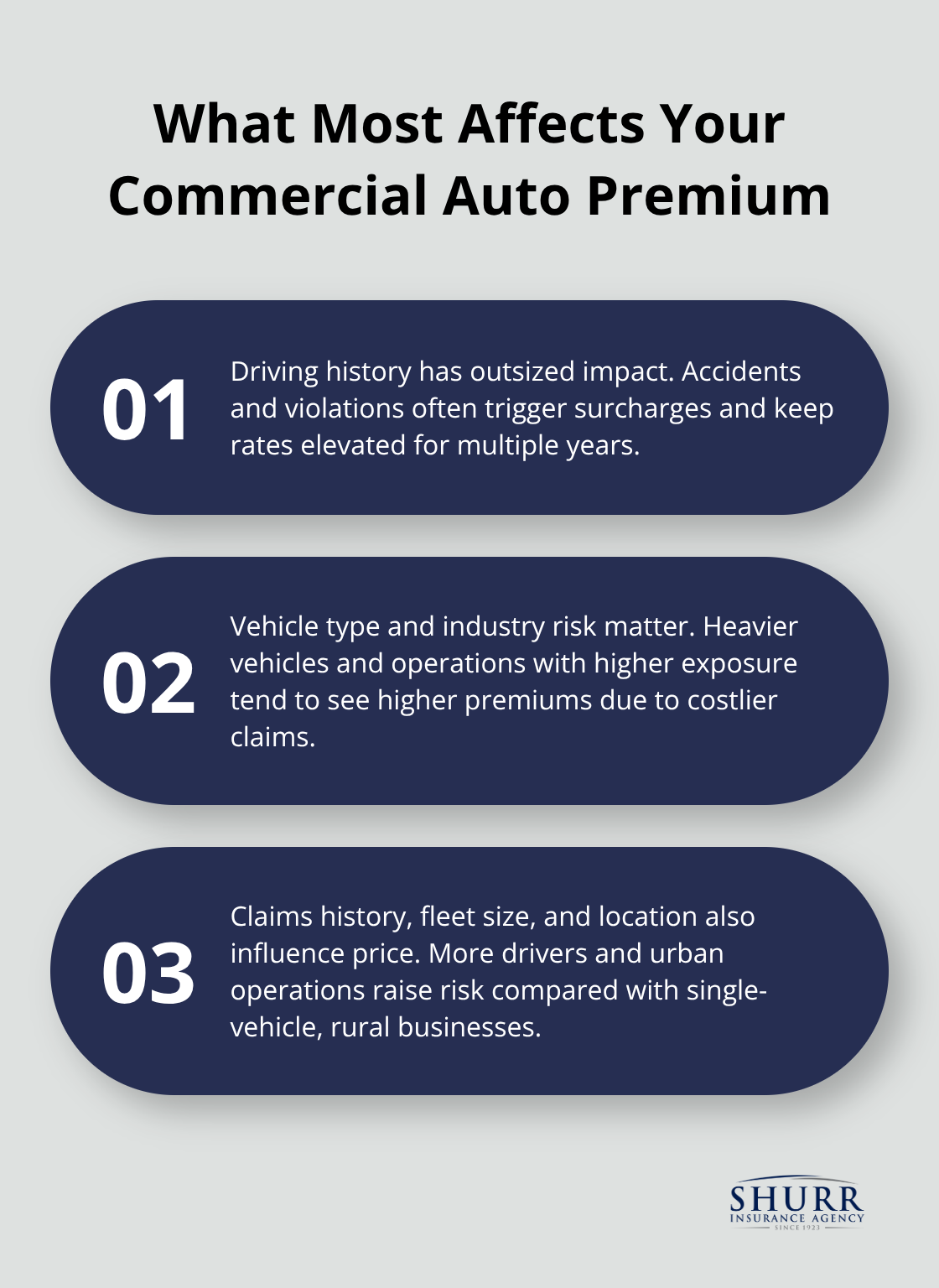

Insurance companies calculate your premium by weighing multiple factors that predict the likelihood you’ll file a claim. The average commercial auto premium runs around $147 per month, or about $1,762 annually, but this baseline shifts dramatically based on your specific situation. Your driving history carries substantial weight in this calculation. Drivers with accidents or violations pay significantly more than those with clean records, sometimes 20–50% higher premiums depending on the severity and recency of infractions.

A single at-fault accident can increase your rate for three to five years.

Vehicle Type and Weight

Vehicle type matters equally in rate calculations. Larger vehicles like box trucks or cargo vans cost more to insure than standard sedans because repair costs are higher and accident severity tends to be greater. A heavy-duty service truck weighing over 15,000 pounds will command a much steeper premium than a compact work van. Your industry classification directly impacts your rate because some industries carry inherently higher risk. Delivery services, construction companies, and transportation-heavy businesses pay more than professional services that use vehicles occasionally.

Claims History and Fleet Size

Claims history stands as the strongest predictor of future claims, so businesses with previous accidents or damage claims face substantially higher premiums going forward. The number of drivers and vehicles in your operation also influences your rate significantly. A sole proprietor with one vehicle pays far less than a small business with three drivers, each with their own driving record to evaluate. Your location matters too because accident frequency, theft rates, and repair costs vary by region. Urban areas typically cost more than rural areas.

Finding Discounts and Optimizing Coverage

When you work with an independent agent, they can identify which factors your insurer weights most heavily and help you understand where you might reduce risk. Some insurers offer discounts for safety training, accident-free years, or bundling commercial auto with other business policies. These discounts can reduce your premium by 10–25%, making the difference between affordable and expensive coverage. An agent can also help you balance coverage limits with cost, recommending higher liability limits if your business contracts require them while avoiding over-insuring areas where you face minimal exposure.

Moving Forward With Your Coverage Strategy

The right coverage at the right price requires understanding your actual risk profile, not just accepting whatever quote you receive first. Once you understand how your specific situation affects your rate, you’re ready to explore what different coverage types actually protect-and which claims scenarios matter most to your business operations.

What Really Happens When You File a Commercial Auto Claim

Liability Claims Protect You From Third-Party Damages

When your business vehicle causes an accident, liability coverage steps in to protect your company from financial ruin. A delivery driver hits another car at an intersection, injuring the other driver and damaging their vehicle. Your bodily injury liability coverage pays the injured driver’s medical bills, lost wages, and pain and suffering up to your policy limit-typically $100,000 or $250,000 depending on what you selected. Your property damage liability covers repairs to the other vehicle. This straightforward liability protection is why carrying adequate liability limits matters enormously. If you only carry the state minimum limit of $25,000 in some states and the accident causes $75,000 in damages, you’re personally responsible for the $50,000 gap. Many businesses carry higher liability limits when their contracts require it, and frankly, it’s smart risk management regardless of contractual obligations.

Collision and Comprehensive Coverage Protect Your Own Vehicle

Collision and comprehensive claims work differently because they cover your own vehicle rather than third-party losses. Your service van strikes a utility pole during a winter storm, causing $8,000 in damage. Collision coverage pays for the repairs minus your deductible, typically $500 or $1,000. Comprehensive coverage handles theft, vandalism, and weather damage like hail or flooding. If your van is stolen from a job site, comprehensive covers the loss. The critical distinction is that collision requires you to be at fault or hit an object, while comprehensive covers losses you didn’t cause.

Medical Payments Coverage Protects Your Employees

Medical payments coverage is where many business owners miss important protection. When your employee gets hurt in an accident, medical payments covers their treatment regardless of fault, typically $5,000 to $10,000 per person. This coverage protects your employees and passengers, paying hospital bills, surgery costs, and rehabilitation without requiring them to pursue a lawsuit. In high-contact industries like construction or delivery services, this coverage prevents employees from suing your business after an accident. Without it, a serious injury claim could cost far more than the medical payments coverage itself would have.

Understanding Your Coverage Needs

Major insurers structure these coverages specifically because claim frequency and severity data shows which scenarios actually happen to businesses. An independent agent understands which coverage types your industry genuinely needs based on real claim patterns, not theoretical ones. When you work with an agent who knows your business operations, they can identify which claims scenarios pose the greatest risk to your company and recommend coverage that actually protects you.

Final Thoughts

Commercial auto insurance protects your business from financial devastation when accidents happen. Understanding how commercial auto insurance works means recognizing that your personal auto policy won’t cover business vehicle use, that your premium reflects your actual risk profile, and that the right coverage prevents catastrophic liability exposure. A single accident can cost tens of thousands of dollars out of your own pocket without proper protection.

An independent agent changes how you approach this decision because they identify which coverage types matter most for your operations rather than accepting whatever quote a large insurer generates. They understand your industry’s specific risks, assess your actual exposure, and recommend limits that protect you without wasting money on unnecessary coverage. An agent also spots opportunities for discounts and helps you navigate claims when they occur, turning a stressful situation into a manageable process.

Contact an independent agent who can review your specific situation and bring details about your vehicles, your drivers, your industry, and how you use your fleet. Shurr Insurance represents many of the best insurance companies in the industry, giving you access to competitive options rather than locking you into one carrier’s approach. A thorough conversation takes 20 minutes and clarifies whether you’re properly covered or carrying unnecessary gaps.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation