Your restaurant’s kitchen equipment is constantly at risk. Fire, water damage, theft, and electrical failures can shut down operations and drain your finances in hours.

Standard commercial policies often leave gaps that leave restaurant owners exposed. At Shurr Insurance, we know that kitchen equipment coverage in Indiana requires specialized protection tailored to your specific operation.

What Counts as Kitchen Equipment Coverage

Kitchen equipment coverage protects the appliances and gear your restaurant depends on daily. This includes refrigerators, freezers, ovens, fryers, dishwashers, walk-in coolers, grills, ventilation systems, and prep tables. When equipment breaks down mechanically or fails electrically, standard property insurance typically refuses to pay. Equipment breakdown insurance fills this gap by covering repair costs, replacement expenses, and the revenue you lose while waiting for repairs. In Indiana, refrigeration failures spoil inventory within hours, and oven failures during peak service hours eliminate your ability to cook and serve customers. A single breakdown can cost thousands in repairs plus thousands more in lost sales.

The Problem with Generic Commercial Policies

Standard commercial property policies cover damage from fire, storms, vandalism, and theft, but they explicitly exclude mechanical and electrical breakdowns. Your property insurance might cost between $1,000 and $5,000 annually in Southeast Indiana, yet it leaves your most expensive kitchen assets unprotected against the failures that happen most often. Restaurant fire claims average around $20,000 per claim, which standard property insurance handles, but equipment failures occur more frequently and still wreck your finances. A refrigerator compressor fails, a deep fryer malfunctions, or an oven control board breaks without warning and without coverage under generic policies. Many restaurant owners learn about this gap only after equipment fails and the insurance company denies the claim.

What Equipment Breakdown Coverage Actually Protects

Equipment breakdown insurance covers the cost to repair or replace kitchen equipment after mechanical, electrical, or refrigeration failures. It also covers the business income you lose while equipment sits broken and waiting for service. If your walk-in cooler fails on a Friday and the repair shop cannot service it until Monday, equipment breakdown coverage pays your lost revenue for those three days. This coverage applies to equipment you own outright or equipment you lease (and it covers both sudden failures and gradual deterioration that finally gives out). When you add equipment breakdown coverage to your property insurance, you create a complete protection layer that addresses the exact risks Indiana restaurant kitchens face daily.

Why Your Kitchen Inventory Needs Separate Protection

Equipment breakdown coverage also protects perishable inventory from spoilage when refrigeration fails unexpectedly. Standard property policies rarely include spoilage protection, leaving thousands of dollars in food and beverages at risk. A power outage or compressor failure can destroy an entire walk-in inventory in hours. Spoilage endorsements attached to equipment breakdown policies reimburse you for the food loss, not just the equipment repair. This distinction matters enormously in Indiana’s restaurant environment, where equipment failures happen without advance notice and inventory loss compounds the financial damage.

How Equipment Breakdown Differs from Property Insurance

Property insurance protects against external events like fire, weather, and theft. Equipment breakdown insurance protects against internal mechanical failures that property policies explicitly exclude. The two coverages work together but serve different purposes. Property insurance might cover a fire that damages your oven, but equipment breakdown covers the compressor failure that stops your refrigerator cold. Understanding this separation helps you identify the gaps in your current coverage and recognize why generic commercial policies leave restaurant owners exposed. Your next step involves assessing which specific equipment in your kitchen poses the greatest financial risk if it fails.

What Threatens Your Kitchen Equipment in Indiana

Fire and Smoke Damage in Restaurant Kitchens

Fire and water damage remain the two most destructive forces in Indiana restaurant kitchens, yet they operate differently than most owners expect. Restaurant fire claims average around $20,000 per claim, and these fires start in cooking equipment far more often than in other areas. Grease buildup in ventilation systems, fryer oil ignition, and electrical shorts in aging ovens cause most kitchen fires. Property insurance covers fire damage from external sources like storms, but it refuses to pay when fire damage involves mechanical failure preceding the flames.

A compressor short-circuit that starts a small fire leaves you unprotected under generic commercial policies. Equipment breakdown coverage protects your kitchen from the internal electrical and mechanical failures that standard policies exclude entirely.

Water Damage from Multiple Sources

Water damage hits harder and faster through multiple pathways: burst pipes in walk-in coolers, roof leaks that drip directly onto electrical panels, flooding from Indiana’s proximity to the Ohio River, and plumbing backups that flood entire prep areas within minutes. Standard property insurance covers water damage from external sources like storms, but it refuses to pay when water damage stems from your own equipment malfunction.

A refrigeration line rupture that floods your storage area leaves you unprotected under generic commercial policies. Equipment breakdown coverage protects against these internal failures that destroy your kitchen’s functionality and spoil thousands of dollars in inventory.

Electrical Failures and Mechanical Breakdowns

Electrical failures and equipment breakdowns occur without warning and without pattern, making them impossible to prevent through security measures alone. A compressor fails on a Tuesday morning during prep, an oven control board burns out during dinner service, or a dishwasher motor seizes without any external cause. These internal mechanical failures destroy your ability to operate for hours or days while waiting for repair technicians.

Equipment breakdown coverage becomes essential because these failures happen frequently, cost thousands to repair, and generate massive revenue loss while your kitchen sits idle. If your walk-in cooler fails on a Friday and the repair shop cannot service it until Monday, equipment breakdown coverage pays your lost revenue for those three days.

Theft and Vandalism of High-Value Equipment

Theft and vandalism of kitchen equipment represents a smaller but concentrated financial risk that many restaurant owners underestimate. High-value items like commercial espresso machines, specialized prep equipment, and portable cooking gear disappear regularly, particularly in urban areas of Northwest Indiana. Standard property insurance covers theft and vandalism, but only if you document the equipment’s value and location accurately.

The real problem emerges when you cannot prove ownership or current condition, leaving insurers to dispute replacement cost claims. Indiana restaurants face all four of these threats simultaneously-fire, water damage, electrical failure, and theft-and each requires different coverage to protect your operation fully. Understanding which specific equipment in your kitchen poses the greatest financial risk if it fails helps you determine the right protection strategy.

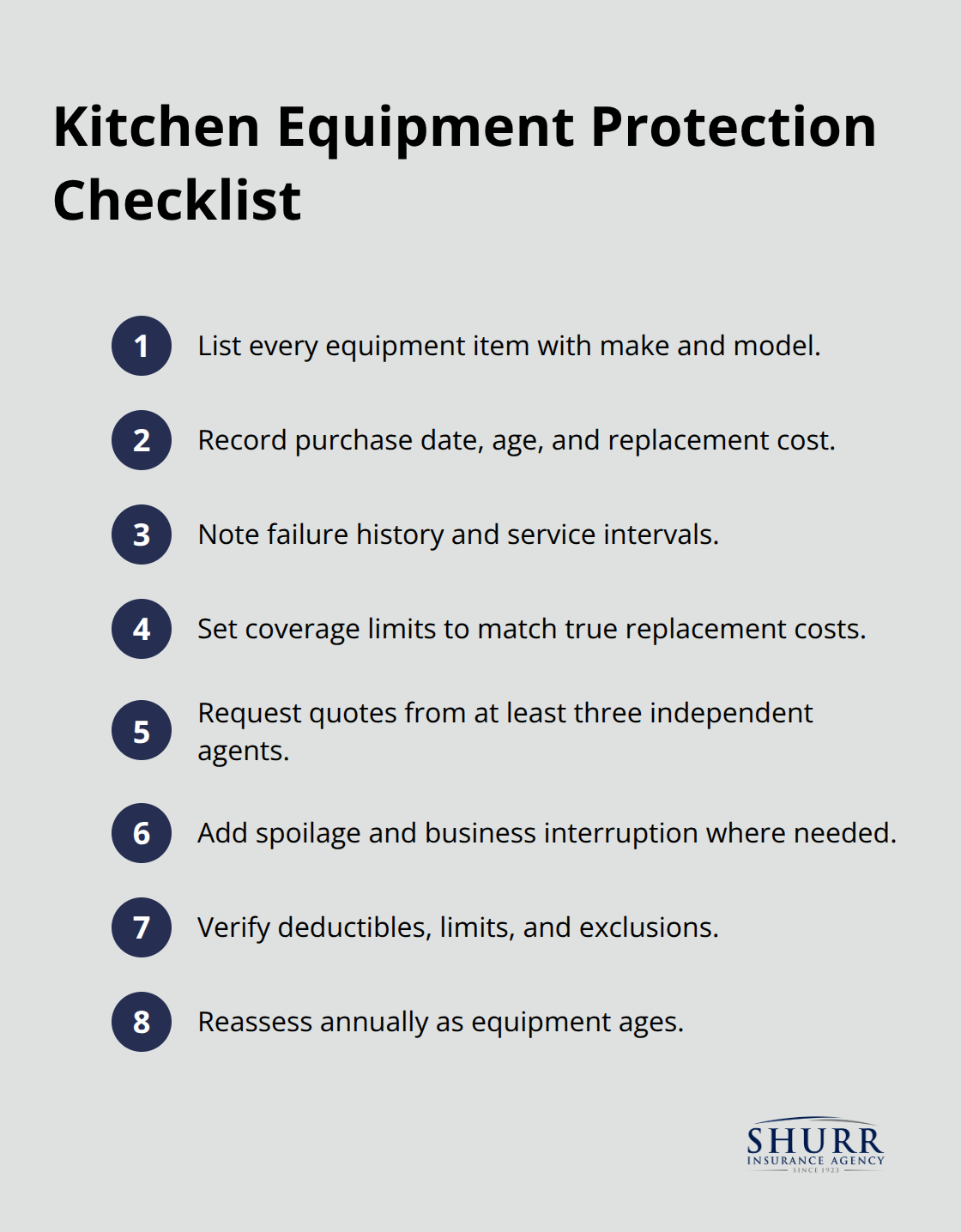

Building Your Kitchen Equipment Protection Strategy

Start by listing every piece of equipment in your kitchen and recording its replacement cost, age, and failure history. Walk through your kitchen with a notepad or spreadsheet and document your refrigerators, freezers, ovens, fryers, dishwashers, walk-in coolers, grills, ventilation systems, and prep tables. Include the purchase date and original cost for each item. This inventory becomes the foundation for determining your coverage limits.

Many restaurant owners guess at replacement costs and end up underinsured, discovering only after a failure that their coverage limit falls thousands short of actual repair or replacement expenses. Equipment breakdown coverage costs roughly $300 to $1,200 annually depending on your equipment’s age and value, making accurate inventory essential to avoid paying for coverage that doesn’t match your actual risk.

Comparing Quotes from Multiple Agents

Contact at least three independent agents who specialize in Indiana restaurants and provide each agent with identical information about your equipment, employee count, annual revenue, building square footage, and whether you offer delivery or serve alcohol. Agents with access to multiple carriers can often secure better rates than captive agents tied to a single insurer. Request quotes within 24 hours and certificates of insurance the same day if you need them quickly for landlords or catering contracts. This comparison process reveals significant price differences and coverage variations that affect your long-term protection and costs.

Identifying Your Specific Kitchen Risks

An independent agent familiar with Indiana restaurant operations will identify risks that generic commercial brokers miss entirely. Ask your agent specifically about equipment breakdown coverage, spoilage protection for perishable inventory, and business interruption insurance that covers lost revenue while equipment sits broken. Mention your cooking methods explicitly-if you operate deep fryers, you face elevated electrical and fire risks that standard policies handle poorly. Indiana’s 2024 tourism pulse brought 83 million visitors spending $16.9 billion statewide, meaning your restaurant likely experiences significant foot traffic and slip-and-fall exposure alongside kitchen equipment risks.

Assessing Flood Risk and Regional Threats

Your agent should assess whether your building’s proximity to the Ohio River increases flood risk, requiring separate flood insurance beyond standard property coverage. Kitchen equipment coverage limits typically range from $500 to $2,000 annually for Indiana restaurants when bundled into a Business Owner’s Policy, delivering better value than purchasing policies separately. Review your current property insurance policy language carefully and verify that equipment breakdown, deductibles, limits, and exclusions align with your operation. Cheaper quotes often miss critical coverages, leaving you exposed to the exact failures that cost thousands monthly in lost revenue.

Taking Action on Coverage Gaps

Contact a specialized Indiana agent to review your current coverage and identify gaps in your kitchen equipment protection. That agent will tailor protection specifically for your kitchen gear and explain how equipment breakdown coverage, spoilage endorsements, and business interruption insurance work together to protect your operation from the financial devastation that equipment failures cause.

Final Thoughts

Kitchen equipment coverage in Indiana protects your restaurant from the financial devastation that equipment failures cause. Fire, water damage, electrical breakdowns, and theft shut down your operation for days or weeks, destroying thousands in inventory and revenue while you wait for repairs. Standard commercial policies leave these risks unprotected, which is why equipment breakdown coverage with spoilage endorsements and business interruption protection becomes non-negotiable for Indiana restaurant owners.

Professional guidance from an agent who understands Indiana restaurants prevents you from purchasing generic policies that miss critical gaps. Your kitchen equipment coverage needs reflect your specific cooking methods, equipment age, inventory value, and regional flood risk. An independent agent identifies which equipment poses the greatest financial threat if it fails and recommends coverage limits that match your actual replacement costs.

At Shurr Insurance, we have served Northwest Indiana restaurant owners since 1923 with insurance tailored to your operation’s unique risks. Our agents build long-term relationships with clients and identify coverage gaps that generic brokers miss entirely. Contact us today to schedule a comprehensive review of your kitchen equipment protection and confirm that your current policies address the exact threats your restaurant faces daily.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation