Owning rental property in Northwest Indiana comes with unique insurance challenges that standard homeowners policies simply don’t address. A Northwest Indiana landlord policy is specifically designed to protect your investment, your income, and your liability exposure.

We at Shurr Insurance see landlords make costly mistakes by assuming their regular homeowners coverage extends to rental units. This blog post walks you through exactly what coverage you need and where gaps typically hide.

What Landlord Policies Actually Cover

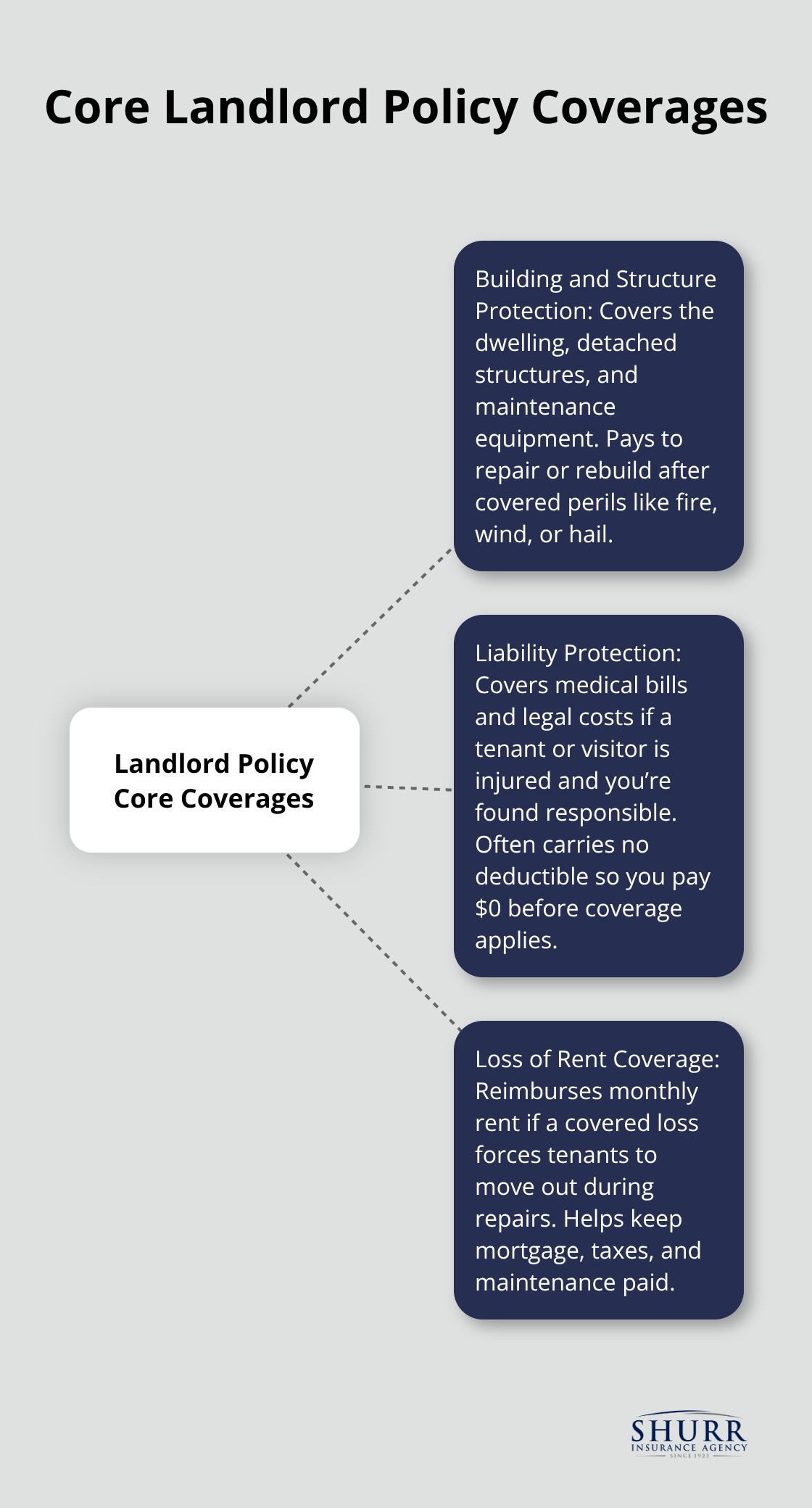

A landlord policy is fundamentally different from homeowners insurance because it protects income-producing property rather than owner-occupied homes. The core coverage includes the building structure itself, liability protection if someone gets injured on your rental property, and loss of rent coverage that keeps your cash flow steady, helping you cover mortgage payments, taxes, and maintenance without tapping into reserves. Property protection covers the physical structure, detached garages, fences, and equipment like lawnmowers or snowblowers used to maintain the rental. Liability coverage handles medical bills and legal expenses if a tenant or visitor gets injured and you’re found responsible.

Loss of rent reimbursement is where landlord policies shine for your cash flow-if fire, hail, wind, or other covered perils damage the property and the tenant can’t live there, the policy pays your monthly rent while repairs happen. This matters enormously because one month of lost rent can exceed your annual insurance premium.

Why homeowners policies fail rental properties

Standard homeowners insurance explicitly excludes rental income and liability exposure that comes with tenants. Insurers view owner-occupied homes and rental properties as completely different risk profiles. Your homeowners policy won’t cover liability claims from tenant injuries, won’t reimburse lost rent during repairs, and often won’t protect the building itself once you rent it out. Many Northwest Indiana landlords discover this gap only after a problem occurs-a tenant’s guest slips on ice, or a pipe bursts and forces a month-long evacuation. The policy they thought covered everything suddenly covers nothing.

What covered perils actually include

Covered perils under landlord policies include fire, hail, wind damage, theft, and vandalism. Liability claims typically carry no deductible, which reduces your out-of-pocket costs when incidents happen. This protection matters because generic coverage leaves you personally liable for these expenses, and medical bills from a single injury can reach tens of thousands of dollars.

How independent agents build the right policy

An independent agent familiar with Northwest Indiana rental properties can build a policy that matches your specific property type, tenant situation, and income needs rather than forcing you into a one-size-fits-all homeowners template. They compare multiple carriers and recommend appropriate liability limits and loss-of-rent coverage based on your actual rental income. This customization is where most landlords realize their previous assumptions about coverage were dangerously incomplete-and where the real protection begins.

Coverage Details Every Northwest Indiana Landlord Needs

Building and Structure Protection

Building and structure protection covers the physical rental property itself-the walls, roof, foundation, and permanent fixtures like built-in appliances. It also extends to detached structures on your property such as garages, sheds, and fences, plus equipment you use to maintain the rental like lawnmowers and snowblowers. Without this protection, you pay personally for repair costs that can easily reach five or six figures after fire, wind damage, or hail. Northwest Indiana experiences significant hail and wind events, making this protection non-negotiable for any serious landlord.

Liability Coverage for Tenant and Visitor Injuries

Liability coverage protects you from financial ruin when a tenant’s guest slips on ice outside your rental or a visitor gets injured on the property. If you’re found responsible, liability pays their medical bills and legal expenses without a deductible, meaning you don’t pay anything out of pocket before the coverage kicks in. A tenant can file a personal injury lawsuit or claim against the landlord’s insurance company for medical bills, lost earnings, pain and other physical damages, and a single lawsuit could bankrupt you without proper protection.

Loss of Rent Coverage During Vacancies or Damage

Loss of rent coverage keeps your mortgage and taxes paid while the property sits unlivable. When fire, hail, wind, or another covered peril damages the unit and the tenant must move out, this coverage reimburses your lost monthly rent until repairs finish. One month of lost rent often exceeds what you pay for a full year of insurance, making this the coverage that actually protects your cash flow.

Getting the Right Dollar Amounts for Your Situation

The real challenge isn’t understanding what these coverages do individually-it’s securing the right dollar amounts for each. An independent agent can review your actual rental income, property value, and liability exposure to recommend specific limits that match your situation rather than generic industry standards. Someone renting a $150,000 duplex needs different coverage limits than an owner with a $400,000 rental home, yet most policies start with the same baseline amounts. This customization directly affects your out-of-pocket costs during a claim and whether you’re actually protected or just partially covered.

With the right coverage amounts in place, most landlords feel confident about their protection. But coverage gaps still hide in the details-and the next section shows you exactly where they appear and how to close them.

Common Gaps in Landlord Coverage and How to Avoid Them

Tenant Belongings Fall Outside Your Policy

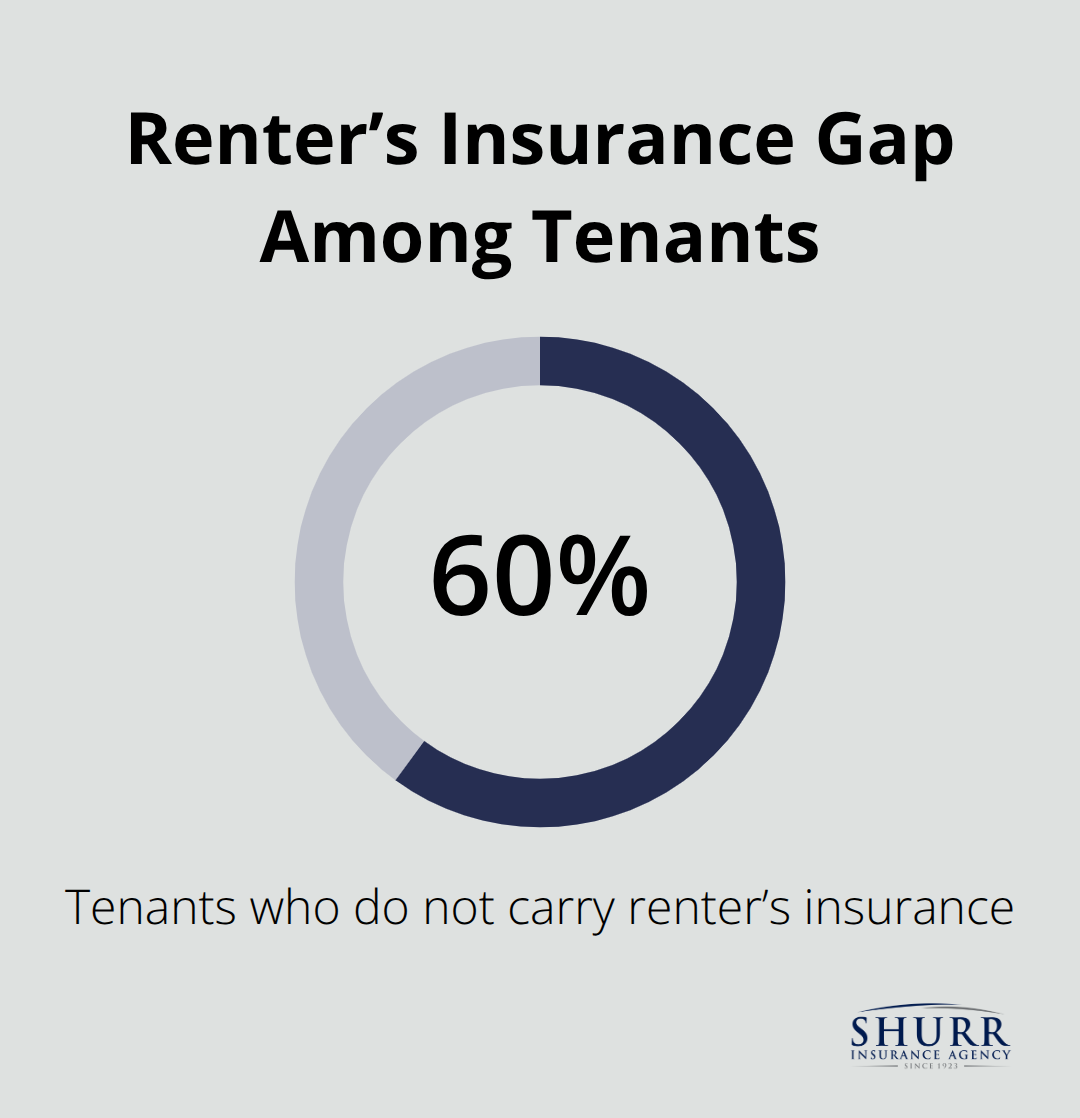

Your landlord policy protects the building and your liability, but it completely ignores your tenant’s belongings. If fire destroys the rental unit, your policy pays to rebuild the structure and covers your lost rent during repairs. Your tenant’s furniture, electronics, clothing, and personal items remain their responsibility through renter’s insurance, which roughly 60% of tenants don’t carry. This creates a dangerous gap: tenants without coverage often pursue claims against the landlord, arguing the property owner failed to maintain safe conditions or that the landlord should have required them to carry insurance.

These disputes become expensive and time-consuming even when you’re not legally liable.

Include a lease requirement that tenants carry renter’s insurance naming you as interested party. This costs tenants about $15 to $25 monthly and protects both parties. Without this contractual requirement, you’ll face angry tenants and potential litigation over property that was never your responsibility to insure.

Specific Damage Types Excluded from Standard Coverage

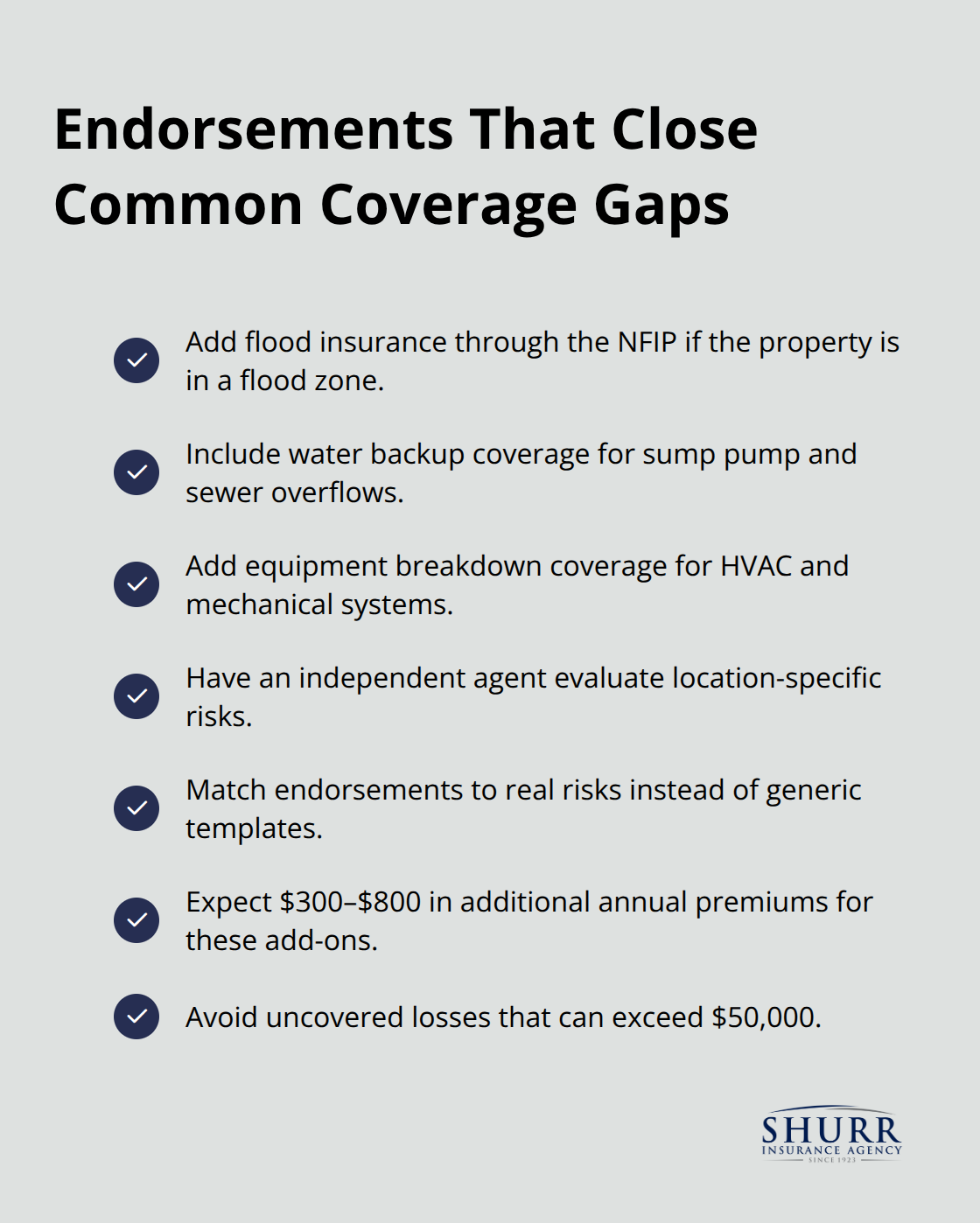

Standard landlord policies exclude specific types of damage that affect Northwest Indiana properties regularly. Flood damage sits outside most landlord policies, yet the region experiences periodic flooding that destroys foundations, mechanical systems, and personal property inside units. Wind and hail damage coverage exists in your base policy, but only up to stated limits, and major storms often exceed those limits. Water backup from sewers or sump pump failure isn’t covered under standard policies despite being common in older Northwest Indiana rental properties. Earthquake and landslide damage are excluded entirely.

Additionally, tenant damage from neglect or intentional acts typically isn’t covered, meaning if a tenant deliberately damages the property or fails to report a water leak for months, you absorb the cost.

Adding Endorsements to Close Coverage Gaps

The solution requires adding specific endorsements to your policy. Flood insurance through the National Flood Insurance Program protects your property if it sits in a flood zone. Water backup coverage provides basement protection. Equipment breakdown coverage protects HVAC systems and other mechanical equipment.

Ask your independent agent to review your actual property location and condition, then add endorsements matching real risks rather than hoping excluded scenarios don’t occur. This proactive approach costs $300 to $800 annually in additional premiums but prevents losses reaching $50,000 or more.

Final Thoughts

A proper Northwest Indiana landlord policy addresses the specific risks you face as a property owner, from liability claims to lost rent during repairs. The gaps between what you think you’re covered for and what actually protects you can cost tens of thousands of dollars when problems arise. Building protection, liability coverage, and loss of rent reimbursement form the foundation of any solid landlord policy, but the real protection comes from matching your coverage limits to your actual property value and rental income.

Schedule a conversation with an independent agent who understands Northwest Indiana rental properties. They’ll review your current situation, identify gaps in your coverage, and recommend specific limits and endorsements tailored to your investment rather than pushing you toward a one-size-fits-all template. This consultation typically takes 30 minutes and costs nothing, yet it often reveals coverage mistakes that could have resulted in five-figure losses.

Contact Shurr Insurance to discuss your landlord policy needs with agents who understand both the insurance details and the local market. We’ll help you build coverage that actually protects your investment and keeps your cash flow steady when problems occur.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation